A business acquisition calculator is not a magic approval button. It is a pressure test. Before you send a lender a package, sign an LOI, or start negotiating with a seller, the calculator should help you answer one plain-English question: does this business appear to produce enough transferable cash flow to support the price and structure you are considering?

That distinction matters because many listings lead with seller discretionary earnings, or SDE, as if it were the buyer’s future take-home cash. It is not. SDE is a starting point for normalized owner benefit. A buyer still has to pay debt service, keep working capital in the business, handle transition mistakes, replace seller-specific labor, and often pay themselves a salary.

The goal of the first screen is not to prove the deal is good. The goal is to find out whether the numbers are strong enough to justify deeper lender, accounting, legal, and operational diligence.

What a calculator can and cannot prove

A good calculator can show whether the asking price, estimated cash down, loan amount, seller financing, buyer salary, and annual debt service fit together. It can also expose when a business that looks affordable is actually fragile after reserves and transition costs.

It cannot verify add-backs, confirm tax returns, judge customer concentration, inspect equipment, predict employee retention, or tell you whether the seller will train you well. It also cannot make a lending decision. SBA 7(a) loans can be used for changes of ownership and working capital, but the lender still underwrites the borrower, business, collateral, industry, valuation, and repayment capacity.

The inputs that matter before a lender call

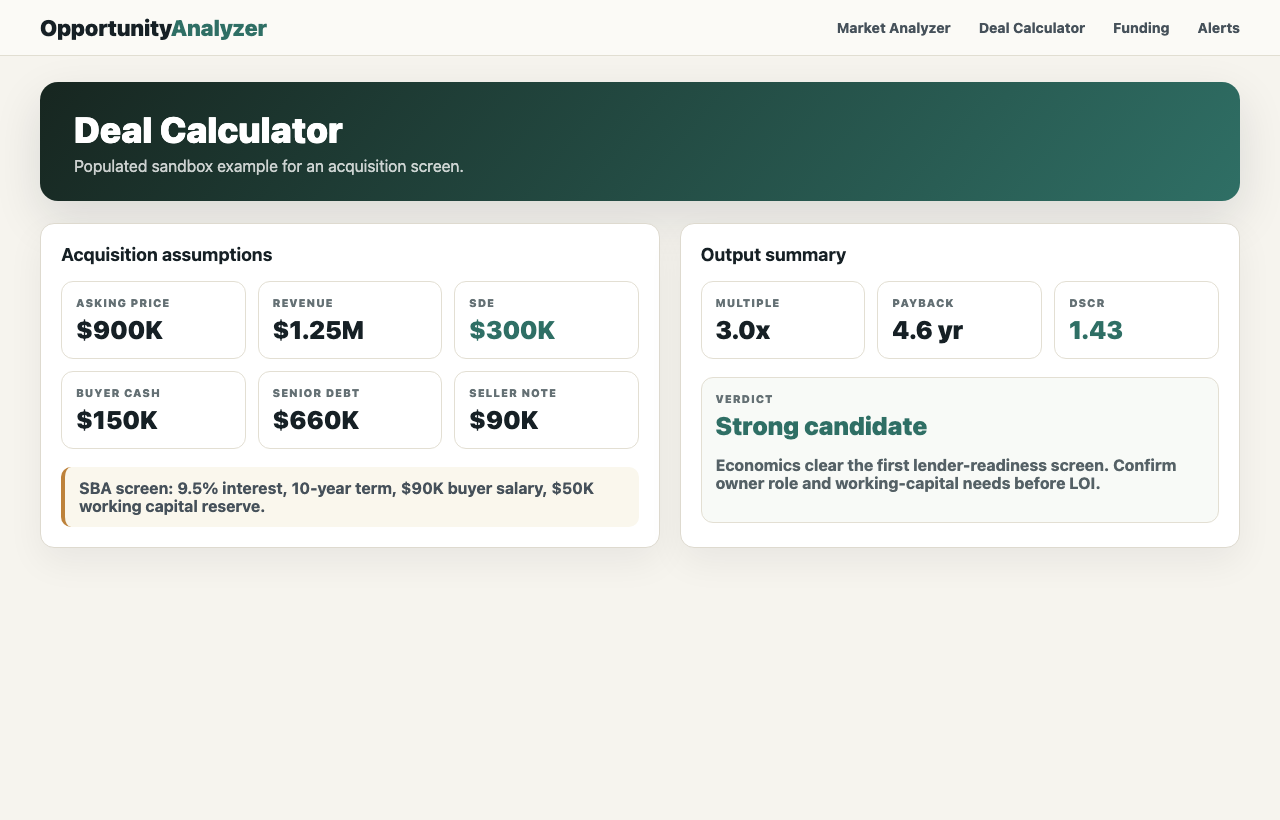

Most weak deal screens fail because the buyer enters too few numbers. Asking price and SDE are not enough. For a first lender-read, you want the calculator to hold the entire proposed structure in one place.

Start with purchase price, normalized SDE, annual revenue, cash down, estimated senior debt, seller note amount, interest rate, term, and whether the seller note is paid monthly, deferred, or on standby. Then add working capital, closing costs, immediate repairs, buyer salary, and a transition-risk cushion.

If the seller says the business has $300,000 of SDE, ask how much of that is supported by tax returns, payroll records, bank statements, and add-back detail. If the listing includes personal expenses, one-time costs, or owner salary adjustments, mark each one as verified, questionable, or unsupported. A calculator is only as useful as the discipline behind the inputs.

Before you trust the output, label the inputs

- Verified: supported by tax returns, bank records, payroll reports, contracts, or invoices.

- Plausible but unverified: reasonable, but still dependent on seller explanations or broker summaries.

- Unsupported: important to the deal math, but not yet backed by documents.

A simple deal screen example

The figure and table below are not valuation rules. They show how quickly acquisition math changes when the buyer accounts for salary, working capital, and debt service. The example assumes the buyer is screening a service business before deciding whether to call lenders.

How the screen moves from listing math to buyer math

The same SDE can tell a very different story after the buyer adds the financing stack and operating cushion.

- Listing SDE$300kSeller-presented cash-flow proxy before buyer adjustments.

- Buyer salary-$90kOwner-operator income needed after closing.

- Senior debt service-$104.6kIllustrative annual payment on senior acquisition debt.

- Pre-tax cushion$105.4kBefore taxes, seller-note payments, capex, and surprises.

Early acquisition screen: illustrative service business

This example uses simple assumptions to show how SDE turns into lender-readiness questions.

| Input or output | Example amount | Why it matters |

|---|---|---|

| Asking price | $900,000 | The headline price before financing structure, working capital, or diligence adjustments. |

| Seller discretionary earnings | $300,000 | Starting cash-flow proxy, subject to verification of add-backs and owner role. |

| Cash down from buyer | $150,000 | Buyer injection for the acquisition, separate from reserves. |

| Seller financing | $90,000 | A 10% seller note may improve alignment, but payment timing matters. |

| Estimated senior debt | $660,000 | Purchase price less buyer cash down and seller note in this simplified example. |

| Illustrative annual senior debt service | $104,600 | Estimated 10-year amortization at 9.5%; actual terms vary by lender and deal. |

| Buyer salary placeholder | $90,000 | The buyer still needs personal income unless outside income covers living costs. |

| Working capital and transition reserve | $50,000 | Cash needed for payroll timing, inventory, deposits, repairs, and surprises. |

| Cash flow after salary and senior debt service | $105,400 | A rough cushion before taxes, capex, seller-note payments, and unexpected issues. |

| Senior-debt DSCR before buyer salary | 2.87x | $300,000 SDE divided by $104,600 senior debt service. Useful but incomplete. |

| Senior-debt DSCR after buyer salary | 2.01x | $210,000 after buyer salary divided by senior debt service. A more conservative early screen. |

The first DSCR looks comfortable because it compares SDE to senior debt service before paying the buyer. The second is more realistic for many first-time buyers because it recognizes that buying a job still requires income. Neither version proves the business is financeable, but the difference tells you which questions to ask before a lender call.

How to read debt service and DSCR

Debt service is the scheduled principal and interest the business must pay on borrowed money. Debt service coverage ratio, or DSCR, compares available cash flow to that required payment. A simple version is cash flow available for debt service divided by annual debt service.

If a business has $300,000 of SDE and estimated annual senior debt service of $104,600, the raw coverage is about 2.87x. But if the buyer needs a $90,000 salary, cash flow before senior debt service becomes $210,000, and coverage falls to about 2.01x. If the seller note also requires immediate monthly payments, the combined coverage falls again.

This is why calculator output is only an early screen. It tells you whether the structure deserves more work. It does not tell you whether the lender will accept the add-backs, whether the valuation supports the price, or whether the business can survive a rocky first 180 days.

Seller financing and working capital

Seller financing can help a deal in two ways. First, it can reduce the senior loan amount or the buyer cash required at closing. Second, it can signal that the seller has confidence in the transition. But the details matter. A seller note that starts amortizing immediately creates real debt service. A seller note on standby may help cash flow early, but the lender and seller have to agree to the terms.

Working capital is just as important and easier to ignore. A buyer may need cash for inventory, payroll timing, rent deposits, insurance, repairs, software changes, slow collections, or a revenue dip after the seller leaves. If all available cash goes into the down payment, the business can be undercapitalized on day one.

When you model a deal, keep three buckets separate: buyer cash invested in the purchase, lender-required reserves or liquidity, and operating cash that stays in the company. Treating them as one pile makes weak deals look stronger than they are.

Transition risk and buyer salary

Many small businesses are still owner-dependent. The seller may handle sales calls, key accounts, scheduling, bookkeeping, vendor relationships, hiring, pricing, or emergency work. If the seller’s role is not replaced, SDE can drop after closing even when revenue looks stable.

A buyer salary is part of that same reality. If you plan to operate the business full time, the business has to support your living needs or you need another documented source of income. A deal that clears debt service only because the buyer takes no salary may be a poor fit for a self-funded buyer.

Before calling a lender, write down the transition jobs that must be covered in the first year: customer handoff, employee retention, bookkeeping cleanup, supplier introductions, license transfers, lease assignment, training period, and any equipment or systems catch-up. The calculator should leave enough margin for that messy work.

When the output is lender-ready

A calculator output becomes useful for a lender conversation when it is paired with evidence. At minimum, be ready to explain the asking price, last three years of revenue and SDE, add-backs, buyer cash down, proposed seller financing, working capital plan, buyer background, transition plan, and why the local market supports the business after closing.

SBA lender documentation reinforces this point. Form 1920 includes change-of-ownership details such as purchase price, buyer injection, valuation, and business broker information. You do not need every final document for a first conversation, but you should know which assumptions are supported and which are still guesses.

What to do next

Use the calculator to decide whether the deal deserves more time. If the screen is weak, change one assumption at a time: lower the price, increase seller financing, defer seller-note payments, increase cash down, reduce buyer salary only if realistic, or walk away. If the screen is strong, your next step is to verify the numbers rather than celebrate the output.

For first-time buyers, the best use of a business acquisition calculator is discipline. It slows the emotional pull of a good listing and turns the conversation into specific questions: What SDE is verified? How much cash stays in the business? What debt service can the company actually carry? What happens if revenue dips during transition? What would a lender need to see before taking this seriously?