Yes, an SBA loan can be used to buy a business in many cases. The more useful question is whether the specific business, buyer, price, and financing structure are strong enough for a lender to underwrite. SBA financing can expand access to acquisition capital, but it does not turn a weak deal into a bankable one.

First-time buyers often hear “SBA loan” and think mostly about down payment. Lenders think more broadly: repayment capacity, buyer liquidity, credit history, management ability, collateral, valuation support, seller transition, industry risk, and whether the business can survive the first year after closing.

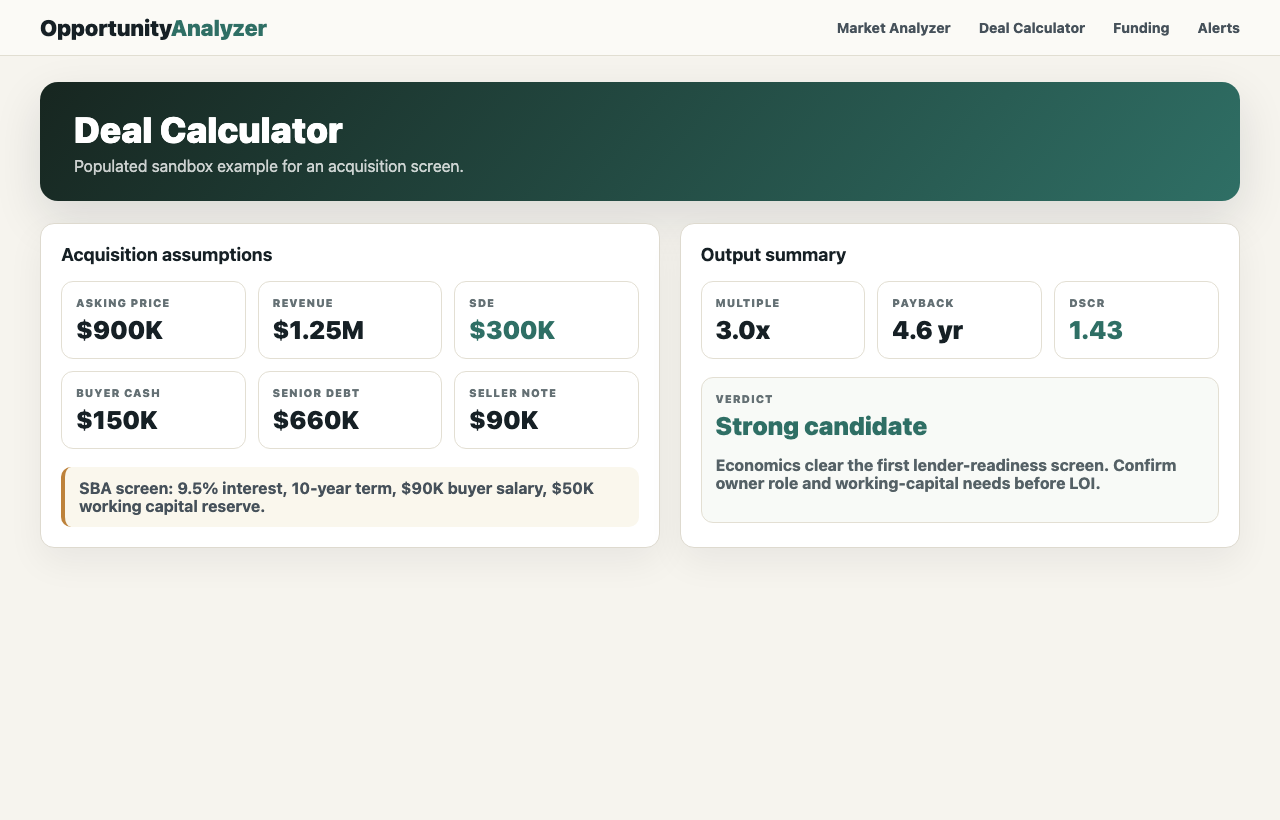

Use this guide before you submit an application. The goal is to understand what lenders will ask for, where deals get stuck, and how to package your acquisition so the first conversation is specific instead of hopeful.

Can you use an SBA loan to buy a business?

The SBA lists changes of ownership among eligible uses for 7(a) financing, along with working capital, equipment, furniture, fixtures, supplies, and other business purposes. That makes 7(a) the SBA program most buyers research first for small business acquisitions.

The same official SBA overview says the maximum 7(a) loan amount is $5 million. That does not mean every buyer can borrow $5 million or that every acquisition qualifies. Loan size, terms, collateral, guaranty, eligibility, and documentation depend on the program type, lender, borrower, and business.

What SBA financing actually does

SBA does not usually lend directly to the buyer. In a typical 7(a) acquisition loan, a participating lender makes the loan and SBA guarantees a portion of it. That guarantee can make lenders more willing to finance eligible small business borrowers, but the lender still underwrites the risk.

For Standard 7(a), SBA describes loans greater than $350,000 up to $5 million, with a maximum SBA guarantee percentage of 75%. For 7(a) Small loans, SBA describes a maximum loan amount of $350,000, with maximum guarantee percentages of 85% for loans up to $150,000 and 75% for loans above $150,000. These program categories can change, so treat the SBA loan type overview as orientation and confirm current fit with the lender.

SBA 7(a) categories buyers often hear about

Use this as orientation only. A lender will tell you which path fits the acquisition.

| Path | Current SBA description | Buyer takeaway |

|---|---|---|

| Standard 7(a) | Greater than $350,000 up to $5 million. | Common path for many acquisition loans above the small-loan threshold. |

| 7(a) Small | Term loans of $350,000 or less. | May be relevant for smaller acquisitions, smaller working-capital needs, or partial financing. |

| SBA Express | Streamlined lender process with a lower SBA guaranty percentage. | May be useful for speed, but not every acquisition fits. |

| Working capital uses | 7(a) can include short- and long-term working capital. | Important because undercapitalized acquisitions can fail even when the purchase closes. |

The lender-readiness screen

A lender-ready buyer can explain the deal in plain numbers: purchase price, SDE, revenue, buyer cash, seller financing, requested loan amount, working capital, closing costs, and why the business can repay debt after the seller leaves.

A lender-ready buyer can also explain themselves. That includes credit history, liquidity, relevant operating experience, management background, outside income if needed, and the plan for taking over customer relationships, employees, vendors, leases, licenses, and bookkeeping.

What lenders are trying to connect

A stronger package connects the buyer, business, financing structure, and transition plan.

- BuyerLiquidityCash injection, reserves, credit, background, and experience.

- BusinessCash flowVerified SDE, add-backs, revenue quality, and industry risk.

- StructureRepaymentSenior debt, seller note, working capital, and collateral.

- TransitionContinuityTraining, staff retention, customer handoff, and operating plan.

Buyer injection, seller financing, and standby debt

Buyers often ask “how much do I need down?” too early. A better first question is how much cash the deal needs across four buckets: buyer injection, closing costs, working capital, and reserves. If you use all available cash for the down payment, you may close into a fragile business.

Seller financing can improve a deal when it reduces senior debt, keeps the seller economically aligned, or gives the buyer more cash flexibility. But seller notes are not all equal. The lender will care whether the note is subordinated, whether payments start immediately, whether it is on standby, how interest accrues, and what happens if the business misses projections.

What documents to prepare

Different lenders will ask for different packages, but the themes are predictable. SBA Form 1919 collects information about the small business applicant, owners, loan request, existing indebtedness, prior government financing, and related eligibility topics. SBA Form 1920 is lender-facing and shows the kind of acquisition details lenders document, including purchase price, valuation, buyer injection, seller financing, collateral, and credit memo items.

Before applying, prepare the basics:

- Three years of business tax returns and financial statements if available.

- Year-to-date profit and loss, balance sheet, and recent bank statements.

- Add-back schedule with support for each claimed adjustment to SDE.

- Purchase agreement or draft letter of intent with price, assets included, and seller note terms.

- Buyer personal financial statement, liquidity proof, resume, and credit explanation if needed.

- Transition plan covering seller training, employees, customers, vendors, lease assignment, licenses, and systems.

What can slow or kill the loan

The most common problems are not mysterious. The seller’s SDE is not supported. Add-backs are aggressive. The buyer has too little liquidity after closing. The seller note starts draining cash too early. The purchase price is hard to support. The lease assignment is uncertain. Key employees or customers may not transfer. Or the buyer cannot explain why they are capable of running the business.

Some problems can be fixed with structure: lower price, more seller financing, deferred seller-note payments, more working capital, better transition support, or a clearer buyer operating plan. Other problems are stop signs. If the cash flow is not real, the seller is evasive, or the business depends on relationships that will not transfer, financing structure will not save the deal.

Early lender red flags and what to ask next

Use this table before spending weeks on a loan package.

| Red flag | Why lenders care | Buyer question |

|---|---|---|

| Weak SDE support | Repayment capacity depends on verified cash flow. | Which add-backs are documented by tax returns, payroll, invoices, or bank records? |

| Thin buyer liquidity | A buyer with no reserves may struggle during transition. | How much cash remains after injection, closing costs, and working capital? |

| Immediate seller-note payments | Total debt service may be too heavy in year one. | Can the seller note be deferred, subordinated, or placed on standby if required? |

| Owner-dependent revenue | Cash flow may not transfer after closing. | Which customer, sales, scheduling, or technical duties sit with the seller? |

| Unclear lease assignment | The buyer may not control the operating location. | What landlord consent, renewal options, and rent increases apply? |

| No buyer operating story | The lender needs confidence the buyer can run the business. | What experience, support, training, or management plan closes the gap? |

How to approach lenders

Start with a lender-read, not a full emotional pitch. You want to learn whether the structure is directionally realistic before you spend heavily on diligence. Bring the acquisition summary, buyer profile, asking price, SDE, cash down, seller financing, working capital estimate, transition plan, and the specific questions you need answered.

SBA Lender Match can connect businesses with lenders, but SBA notes that using Lender Match does not guarantee a match or loan offer. Whether you use Lender Match, a local bank, a lender marketplace, or a referral, compare how lenders think about your industry, deal size, collateral, seller note, timeline, and documentation standards.

What to do before applying

Before you apply, run the deal through a basic acquisition calculator, collect the seller’s financial support, and write a one-page lender summary. If the first screen is weak, improve the structure before sending a package. If the first screen is strong, use lender feedback to identify the next documents and diligence questions.

An SBA loan can be a powerful acquisition tool, but it is still debt. A first-time buyer should treat the application as a test of the deal’s evidence, structure, and transition plan. The better prepared you are before the first lender call, the faster you will learn whether the business deserves serious pursuit.