A small business valuation multiple is a shortcut. It is not the valuation. Buyers usually hear a business is listed at “three times SDE” and start debating whether that multiple is fair. The better first question is whether the SDE is real, transferable, and enough to support the buyer’s financing and salary. The AICPA Business Reference Guide is one example of a professional reference buyers may encounter when researching rules of thumb and SDE-based valuation context.

Published multiple data can help orient a buyer, but it should not replace deal-specific diligence. IBBA and M&A Source Market Pulse reports separate smaller Main Street transactions from lower-middle-market deals, which is exactly why buyers should avoid mixing small-business SDE multiples with larger-company EBITDA multiples.

Start with transferable earnings

A buyer is not buying the seller’s past lifestyle. The buyer is buying the future cash flow that can transfer after closing. If the seller personally drives sales, holds licenses, maintains key relationships, or works 70 hours a week without market-rate replacement cost, SDE may overstate what the buyer gets. Exit Planning Institute frames transferable value around human, structural, customer, and social capital, which is a useful lens for buyer diligence too.

Normalize SDE carefully

SDE usually starts with profit and adds back owner compensation, discretionary expenses, interest, depreciation, amortization, and non-recurring items. Each add-back needs evidence. Some seller expenses are legitimate add-backs. Others are simply operating costs that will continue after closing.

Add-back review table

Label each add-back before accepting normalized SDE.

| Add-back type | Often reasonable when | Buyer caution |

|---|---|---|

| Owner salary | The buyer will replace the owner and salary is already counted correctly. | A buyer still needs salary or replacement management cost. |

| Personal auto/travel | Clearly personal and not needed for the business. | Some vehicle/travel cost may continue for sales or operations. |

| One-time legal or repair | Documented and truly non-recurring. | Deferred maintenance may recur after closing. |

| Family payroll | Person did not work in the business. | If family member performed real work, replacement labor is needed. |

| Rent adjustment | Market rent is clearly different from current rent. | Lease renewal may reset economics. |

A multiple is a shorthand, not a verdict

The same multiple can be cheap or expensive depending on risk. A business with clean records, recurring revenue, strong staff, low capex, and low owner dependence can justify a stronger valuation than a business with unsupported cash sales, customer concentration, immediate repairs, and a short lease.

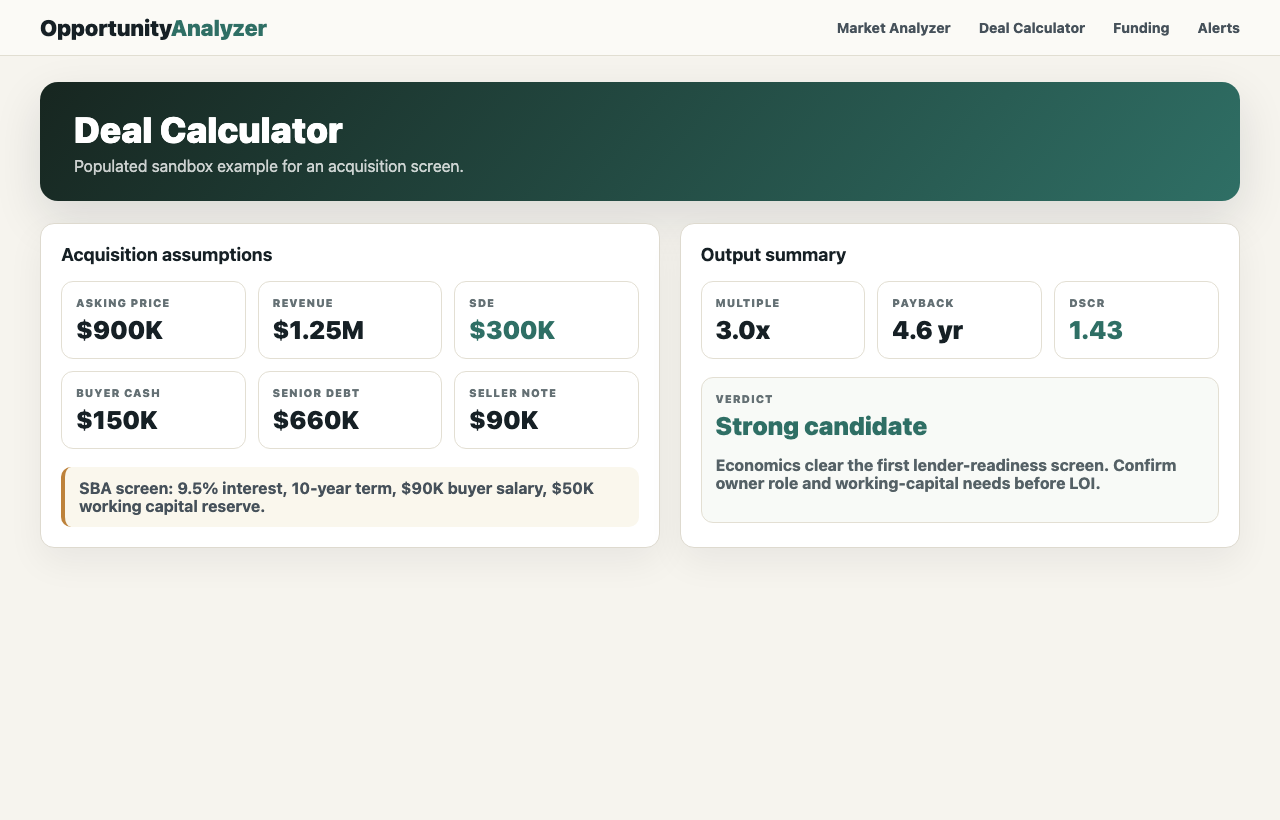

Run buyer cash-flow math

After estimating value, run the acquisition as a buyer. Include purchase price, cash down, seller financing, senior debt, interest rate, amortization, working capital, buyer salary, closing costs, and first-year transition cushion. SBA lender documentation asks lenders to capture items such as purchase price, buyer injection, seller financing, and valuation, which is a useful reminder that price and structure are evaluated together.

Adjust for risk before making an offer

Valuation is not only about the number. It is about structure. A buyer can reduce risk with a lower price, seller financing, earnout-like contingent payments where appropriate, repair escrow, inventory true-up, lease contingency, training period, or working-capital adjustment.

The structure should match the risk you found. If the risk is revenue transfer, a longer seller transition or contingent component may matter more than a small price reduction. If the risk is equipment, a repair escrow or capex adjustment may be cleaner. If the risk is lender coverage, the solution may be more equity, seller standby, or a lower price.

Do not let a seller or broker force every diligence concern into a single multiple debate. Serious buyers translate each concern into one of four places: price, terms, conditions, or walk-away criteria.

If you cannot verify earnings, transfer customer relationships, keep key employees, or finance the deal with enough cushion, the right valuation may be no offer.