Seller financing can make a small business acquisition more realistic, but it can also make a weak structure look better than it is. A seller note is not free money. It is debt, alignment, negotiation leverage, and transition risk sharing rolled into one document. SBA-related seller-note treatment can change with program rules, so buyers should verify current requirements in SOP 50 10 and with their lender before relying on any structure.

What seller financing does

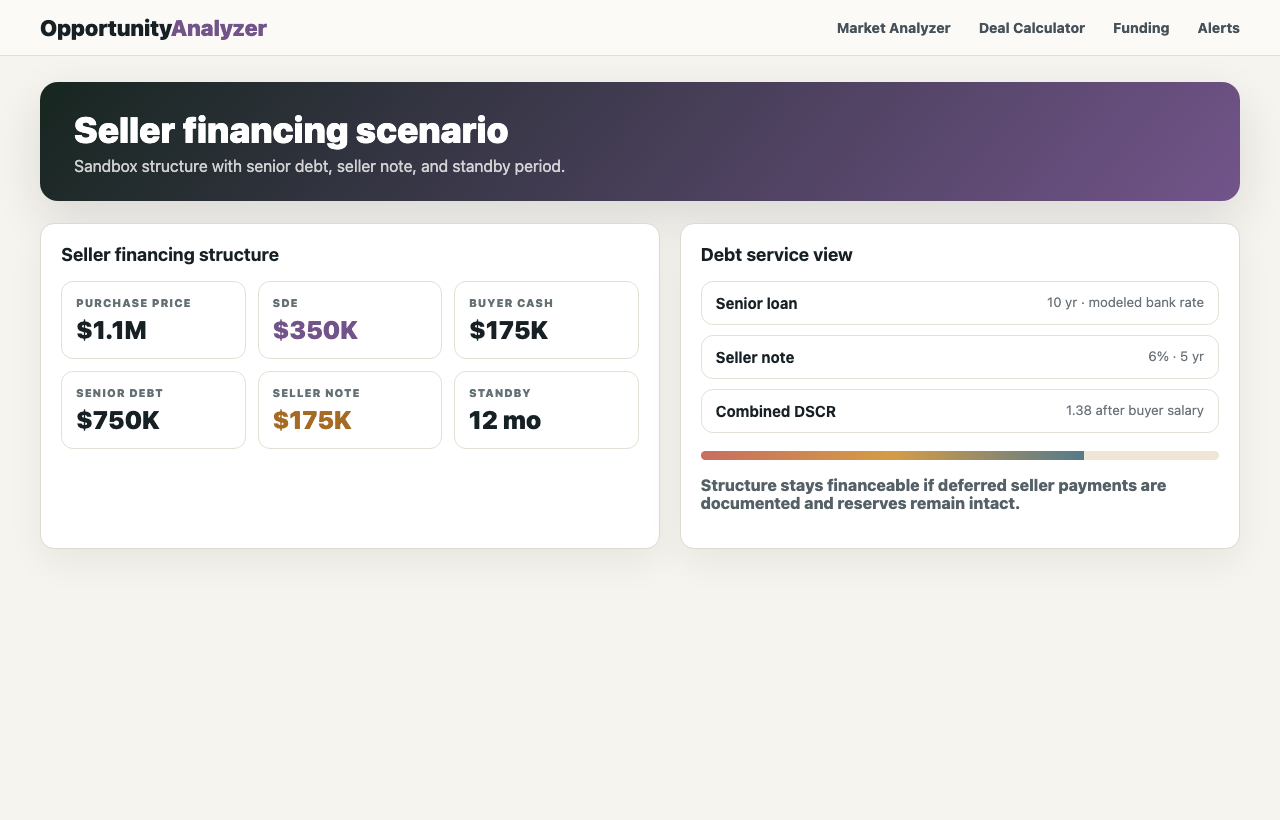

Seller financing means the seller accepts part of the purchase price over time instead of receiving all cash at closing. That can reduce buyer cash pressure, lower senior debt, and keep the seller economically tied to a successful transition.

Terms that matter more than the note amount

A $200,000 seller note can mean very different things depending on term, interest rate, amortization, payment start date, balloon, standby requirements, collateral, default rights, and subordination to senior debt. Buyers should model the exact payment schedule, not just the headline note size. SBA lenders may also apply specific standby or subordination expectations; NAGGL program notices are useful context, but lender counsel should confirm the actual loan structure.

Seller note terms to screen

These terms change both lender readiness and buyer risk.

| Term | Buyer question | Why it matters |

|---|---|---|

| Payment start | Do payments begin immediately or after a standby period? | Year-one cash flow can change materially. |

| Amortization | Is the note amortizing, interest-only, or balloon-heavy? | Cash drain and refinance risk differ. |

| Subordination | Does senior lender require the seller to sit behind the bank? | Can affect lender approval and seller negotiation. |

| Security | What collateral or remedies does the seller have? | Affects downside risk if the business underperforms. |

| Transition obligations | Is seller help tied to the note or documented separately? | Training and handoff should be explicit. |

How seller financing changes debt service

A seller note can improve the senior-loan screen by reducing the bank debt needed at closing. But if the note also requires immediate payments, total debt service may still be too high. Run the acquisition three ways: senior debt only, senior debt plus immediate seller note, and senior debt plus deferred or standby seller note.

Lender readiness and SBA context

SBA 7(a) financing can be used for changes of ownership, but lenders still underwrite repayment capacity and structure. Lender-facing SBA Form 1920 includes acquisition details such as purchase price, buyer injection, seller financing, valuation, and collateral. That is a reminder that seller financing is part of the underwriting story, not a side agreement to ignore.

How to use seller financing in an offer

Use seller financing to solve specific deal problems. If transition risk is high, ask for more seller financing and stronger training obligations. If senior debt is too high, ask for a seller note that reduces bank leverage. If year-one cash flow is tight, discuss deferred payments or standby terms where appropriate.

The offer should describe the business reason for the note. A note tied to transition support sends a different message than a note used only because the buyer lacks cash. A lender, attorney, and seller will all want to understand how the note interacts with security, default rights, senior debt, and post-close operating needs.

Buyers should also model what happens when the standby or deferral period ends. A structure that looks comfortable in year one can become tight in year three if seller-note payments begin before revenue growth, margin improvement, or debt paydown has actually happened.

The right seller note is not the largest one. It is the one that creates enough alignment, preserves enough cash flow, and fits the lender’s structure while giving both buyer and seller a reason to make the transition work.